Saying that millennials’ pursuit of homeownership is filled with obstacles is an understatement.

Saddled with copious student debt while facing fast-rising property prices, saving up 20% down payments often seems unattainable for your twenty- and thirty-something buyers.

But with careful consultations and coaching grounded in realistic expectations, creative problem-solving, hyper-localization knowledge, and unrelenting determination, you can still successfully guide more young clients to one day realizing primary residence purchases.

Yes, pre-approvals will get denied and winning bids lost at first.Yet by maintaining trust-based partnerships where guidance continually aligns evolving life goals with budget trade-offs, the numbers can slowly shift in your clients’ favor over time.

The key is meeting millennials where they stand financially, then build sustainable roadmaps tailored to reaching individual homeownership.

Chapter 1: The Challenges of Millennials and Home Ownership

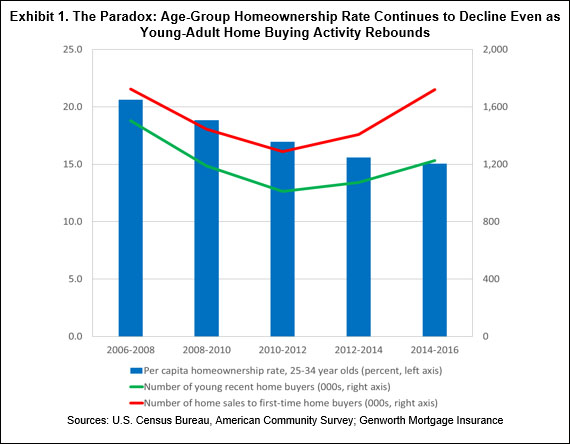

Millennials, defined as those born between 1981 and 1996, face unique barriers when it comes to homeownership compared to previous generations. The chart below says it all:

Source: Fannie Mae

Among Millennials, homeownership rates have been on the decline even though the number of home purchases by young adults and first-time buyers is on the rise, and the trend is still going strong to this day.

The reality is, despite a strong desire to own property, several key factors have severely hampered millennials' ability to enter the housing market.

Financial Constraints

The most significant roadblock for millennials hoping to buy their first home is a lack of financial resources.

Compared to baby boomers and Gen Xers when they were the same age, millennials have much lower incomes and net worths on average. There are two things here that work hand in hand:

Wage growth has been stagnant for young workers over the past few decades.

At the same time, housing prices have risen rapidly, resulting in a widening gap between incomes and home values.

This makes it incredibly difficult for millennials to save up enough money for a down payment.

Even those with decent incomes struggle to qualify for mortgages unless they have family assistance.

High Student Loan Debt

In addition to low incomes, millennials also have the highest student loan debt of any previous generation.

Over 50% of millennials pursuing a bachelor's degree take out student loans, with an average balance of nearly $30,000.These student debt burdens delay millennials' timeline for buying homes by forcing them to allocate large portions of their income toward monthly loan payments rather than saving.

Paying off student loans can prolong the home-buying process by years or even decades.

Competing in Tough Housing Markets

Millennials often live and work in some of the country's most competitive real estate markets, like New York, Los Angeles, and San Francisco.

Not only do these areas have extremely high home prices, but inventory is very limited.

Cash offers and bidding wars are common, making it nearly impossible for first-time home buyers on a budget to win out.

As a result, the homeownership rate among millennials in high-cost urban areas is dismally low.

Barriers to Mortgage Approval

Even when millennials finally feel financially ready to buy a home, getting approved for a mortgage can be another major obstruction.

Most lenders require a minimum credit score of around 620 for an FHA loan or 680 for a conventional loan.But according to Experian, the average millennial credit score is just 638.

Poor credit combined with high debt-to-income ratios from student loans causes many to fall short of qualifying for home loans.

Chapter 2: How Millennials Can Afford to Buy a Home

Despite mounting barriers, homeownership remains an important life goal for most millennials.

With careful planning and patience, they can overcome the financial hurdles to buying their first property.

Here are practical tips for how millennials can improve their chances of homeownership.

Pay Off Debt

Before applying for a mortgage, millennials should focus aggressively on reducing debt from student loans, credit cards, auto loans, and personal loans.

Lenders need to see manageable monthly debts compared to income.

Paying down balances directly raises credit scores too.

Consider contacting servicers to adjust payment plans if needed.

Build Emergency Savings

On top of paying off high-interest debt, millennials should start building their emergency fund.

Saving enough to cover 3-6 months of living expenses reassures lenders that they can continue making mortgage payments during unexpected financial hardships. It also provides a down payment buffer.

Enroll in First-Time Homebuyer Programs

Many state and local governments offer special programs to encourage and assist first-time home buyers.

These can include subsidized mortgages, discounted interest rates, waived origination fees, lowered down payment requirements, and even direct grants for closing costs or down payments.

Millennials should thoroughly research what homebuyer assistance programs are accessible to them and how to qualify.

Leverage Low Down Payment Loans

Traditional 20% down payments on home purchases are unrealistic for most millennials.

Luckily, FHA loans only need 3.5% down, and many big lenders now offer conventional loans with 5% down. VA and USDA loans sometimes need no down payment whatsoever if the borrower meets eligibility rules. Shopping multiple lenders for the lowest PMI rates and fees on small down payments is key.

Consider Relocating

If able to move for work, millennials in ultra-expensive housing markets could relocate to more budget-friendly metro areas to expedite homeownership.

Cities like Pittsburgh, St. Louis, Atlanta, Houston, Salt Lake City, Raleigh, and Minneapolis all offer reasonable home prices while still providing urban conveniences and plentiful jobs.

Team Up with Family or Friends

Jointly purchasing a home with other first-time buyers makes the process much more feasible.

Combining incomes, savings, and buying power allows co-buyers to afford move-in ready homes they may not have been able to alone.

Investing in real estate with family often increases chances of getting gifted money for closing too.

MaverickRE:

The data-driven real estate platform that skyrockets your business through predictability, efficiency and control.

Chapter 3: Tips for Millennials Looking to Become Homeowners

For millennials seeking the financial and lifestyle benefits of homeownership, here is specific guidance tailored to overcoming the unique obstacles they face:

Improve Credit Scores

Boosting credit should be priority number one.

On-time payments, low card balances, credit mix, and account history all factor into the scoring algorithms.

Dispute and correct any errors on credit reports for quick score jumps too.

Shooting for at least 680 establishes home loan eligibility.

Craft a Household Budget

Create a realistic budget that allows for aggressively paying down debts, saving up a down payment fund, and covering mortgage principal, interest and escrows in retirement.

Make sure to include room for unplanned expenses without breaking the bank.

Ask lenders to review draft budgets for approval.

Get Pre-qualified

Shop lenders and apply for mortgage pre-qualification letters, which verify eligibility and loan amounts based on a soft credit check.

Being armed with a pre-approval in advance makes competitive offers more desirable to sellers.

Locking in rates early shields against unpredictable rate swings too.

Line Up Down Payment Help

In addition to personal savings, explore other sources like family gifts, employer programs, special mortgage options, and state/local down payment assistance grants.

Every little bit helps reduce high monthly payments and avoid draining every last dollar of reserves when buying.

Attend Homebuyer Education Courses

Sign up for first-time buyer workshops, seminars, and housing counselling to gain knowledge before entering the market.

Learning about tax deductions, insurance, real estate agents, regulations, laws, mortgage options, and more leads to smarter purchasing selections.

Prioritize Energy Efficiency

Focus the property search on newer builds or newly renovated homes boasting efficient construction techniques, updated HVAC systems, ample insulation, modern appliances, smart home tech, etc.

Energy savings make budgeting easier, and low utility bills directly raise borrowing power.

Ask Sellers to Cover Closing

Leverage low housing inventory to negotiate seller concessions for covering some or all closing costs and prepaids.

This preserves precious cash otherwise sunk into appraisal gaps, origination charges, prepaid property taxes and insurance, and more.

Inspect Before Committing

Refuse to waive contingencies that allow for professional home inspections and appraisals prior to finalizing deals.

Don't get stuck with expensive repairs or overpaid purchase prices that stretch budgets too thin.

Push back on asbestos, knob and tube wiring, foundation cracks, pest infestations, and faulty systems.

Renew Leases If Needed

There is no shame in waiting another year or more rather than depleting every last penny to barely scrape together a problematic purchase.

Renew apartment leases and stick to money-saving rent budgets until reaching prime financial homeownership readiness. Patience pays off.

Embrace Persistence

Stay determined and proactive despite repeated denied loan applications or failed offers in hypercompetitive markets.

With financial discipline and strategic optimism, the barrier-breaking day when keys finally get handed over draws nearer every passing year.

Homeownership can still thrive in millennials’ futures.

Chapter 4: Key Takeaways for Real Estate Agents

For real estate professionals seeking to boost millennial home buying business, certain tips and best practices stand out:

Know Their Priorities

Get to know top desires like move-in readiness, pet friendly spaces, hi-tech features, commutable locations, vibrant communities, and potential rental income.

Cater listing recommendations around these. Balance wishes with budget realities respectfully.

Promote Down Payment Help

Ensure millennials are informed on down payment assistance programs, seller concessions, loan types requiring less cash down, and ways to receive family gifts.

When preapprovals fall short, provide credit counseling referrals to improve mortgage-worthiness over time.

Strategize Within Budget

Guide clients through the pre-qualification process to determine affordable price ranges, then strategize the best allocation of their savings and gift funds toward overbid prices, covering appraisal gaps, or out-of-pocket closing costs and prepaids.

Help set expectations on trade-offs.

Lean On Lender Relationships

Maintain trusted lender partnerships that will collaborate to structure more creative financing solutions for qualified millennials who fall just shy of approval thresholds.

Offer connections to loan officers go the extra mile to make deals work.

Align Life Goals

Keep big picture lifestyle priorities front and center, not just housing dreams.

Help clients balance trade-offs between home locations, sizes, ages, layouts and amenities with budgets, commutes, childcare needs, and retirement savings goals.

Provide Ongoing Education

Offer free first-time buyer courses, host housing counsellors to speak at open houses, distribute pre-purchase checklists, and share budget calculators or money-saving tips.

Position your team as patient educators, not just salespeople.While minority millennials still struggle greatly with home ownership compared to previous generations, fine tuning personalized advisory services for young clients can steadily help more achieve turning the key of their own front door at long last.

Turn Millennial Renters into Happy Homeowners With Ylopo

Getting millennials to finally secure homeownership can often seem impossible.

Yet with Ylopo as your ally providing state-of-the-art real estate technology and digital marketing expertise cultivated from over 50 years of industry experience, even the biggest barriers start to crumble.

Our automated branded site builder, AI-powered lead gen and nurture tools, and geo-targeted ad campaigns specifically attract and convert more first-time millennial buyers by aligning with their unique priorities and budget realities every step of the way.

Don't let another promising young client's dreams of owning slip through the cracks.

Book a demo now to unlock Ylopo's comprehensive sales-accelerating, customer-winning solutions focused on opening the door to sustainable millennial homeownership.

About the Author

Aaron “Kiwi” Franklin

Head of Growth

Aaron "Kiwi" Franklin is the Head of Growth at Ylopo and an innovative technologist and serial entrepreneur who has over 25 years of experience creating digital solutions for major brands and pioneering companies at the intersection of technology and real estate. His depth of expertise stems from leading development of the first website for Apple to founding a global community of over 1,000 elite athletes. Connect with me